As you approach retirement, one of the most pressing concerns you may face is how market volatility will impact your retirement savings.

Market volatility refers to the frequent and sometimes unpredictable ups and downs in the stock market. These fluctuations can significantly influence your retirement portfolio, especially if you are nearing or in retirement. Understanding how to navigate this volatility is crucial for high-net-worth individuals (HNWIs) who want to preserve their wealth and secure their financial future.

In this blog, we’ll explore how market volatility affects retirement savings, strategies to safeguard your wealth, and how financial planning with CKS Summit Group can help mitigate risks during turbulent times.

Understanding Market Volatility

Market volatility is often measured by the CBOE Volatility Index (VIX), which tracks the expected volatility of the stock market. While some market fluctuations are normal, larger swings can have a more significant impact on retirement portfolios. During periods of high volatility, such as the 2008 financial crisis or the more recent COVID-19 pandemic, stock prices can drop rapidly, creating fear and uncertainty for investors.

According to a recent study, missing just the 10 best trading days in the market over a 20-year period could significantly reduce your portfolio’s overall return. Market timing is often a losing game, so it’s essential to maintain a long-term perspective, particularly in retirement.

Why Market Volatility Is a Concern for Retirees

When you’re still working, you have time to recover from market downturns. You can continue contributing to your retirement accounts, buying assets at a lower price during a downturn, and potentially benefiting from a market rebound. However, once you retire, your ability to ride out market declines diminishes, as you may need to withdraw from your savings to cover living expenses.

This creates a situation known as the sequence of returns risk, which occurs when you withdraw money from your retirement accounts during a market downturn. If your portfolio loses value and you continue to make withdrawals, it becomes harder for your savings to recover, potentially leading to a shorter retirement horizon.

Real-World Impact of Market Volatility on Retirement

Consider the following example: If an individual’s portfolio is invested heavily in stocks and the market drops by 20%, their portfolio could lose a fifth of its value. If they were planning to withdraw 4% per year for living expenses, this withdrawal rate becomes a higher percentage of the now reduced portfolio, further accelerating depletion. This is a scenario many retirees encountered in 2008 and more recently in 2020 during the pandemic.

The Employee Benefit Research Institute reports that Americans who experience significant market losses within the first five years of retirement could see a 20% reduction in their overall retirement income potential. For wealthy individuals, this impact is more about protecting legacy wealth and ensuring that you can live the lifestyle you’ve worked hard to achieve throughout your retirement.

Strategies to Protect Your Retirement Savings During Volatile Markets

Given the risk that market volatility poses to your retirement savings, it’s important to adopt strategies that protect your wealth while allowing for some growth. Here are some strategies to consider:

1. Risk Tolerance Assessment

Before deciding how to allocate your portfolio, it’s essential to assess your risk tolerance. As you near retirement, your risk tolerance generally declines because you have less time to recover from market losses. Work with your financial advisor to determine a risk level that you’re comfortable with, and adjust your portfolio accordingly.

At CKS Summit Group, we advocate for regularly reassessing your risk profile, especially when market conditions change or as you enter new life stages. A financial plan that worked for you in your 40s or 50s may not be as effective as you approach or enter retirement.

2. Fixed-Income Investments

Fixed-income investments are less volatile than stocks and can provide a stable source of income during retirement. However, it’s important to monitor interest rates, as rising rates can reduce the value of existing bonds.

According to the Federal Reserve, recent interest rate cuts signal a shift in monetary policy aimed at stabilizing economic conditions. While rates may still fluctuate, lower interest rates can lead to reduced yields on traditional fixed-income investments. This makes it crucial for retirees to carefully consider how to allocate their assets.

Fixed annuities, which provide a guaranteed income stream regardless of market conditions, can be an attractive option for those looking to help secure stable cash flow and reduce their exposure to market swings. Incorporating these investments into a balanced portfolio can help manage risk while navigating a low-interest-rate environment.

3. Diversification

Diversification is a fundamental principle in retirement planning, especially during volatile markets. Spreading your assets across various sectors, asset classes, and geographical locations can help reduce your exposure to any single investment’s downturn.

High-net-worth investors often benefit from diversifying not just within stocks and bonds but also into alternative investments like real estate, private equity, or commodities. This broader diversification can help cushion the blow from a stock market downturn and offer other opportunities for growth when traditional markets falter.

4. Bucket Strategy

The bucket strategy is another way to help protect your savings from volatility. This approach involves dividing your retirement assets into different “buckets,” each with varying levels of risk. The first bucket is designed for short-term needs and is filled with liquid, low-risk investments like cash or short-term bonds. The second bucket is for medium-term expenses and might include balanced funds or conservative stock investments. The third bucket is for long-term growth and can contain higher-risk investments like equities.

This strategy helps ensure that during market downturns, you can withdraw from the low-risk bucket while leaving your higher-risk investments to recover over time.

5. Stay the Course and Avoid Panic Selling

Emotional decision-making can be your worst enemy during volatile markets. One of the biggest mistakes retirees make is panic selling during a market downturn, locking in losses and missing out on potential market recoveries.

A study by Dalbar Inc. showed that the average investor significantly underperforms the market, primarily due to poor timing decisions driven by fear or greed. Maintaining a disciplined, long-term investment strategy is key to weathering periods of volatility.

6. Consider Hiring a Pro

Working with a financial advisor is critical, especially during periods of market turbulence. An experienced advisor can help you craft a retirement strategy that is resilient to market volatility, incorporating tax-efficient withdrawal strategies, and helping ensure your portfolio is aligned with your long-term goals.

At CKS Summit Group, our advisors have extensive experience working with high-net-worth individuals, helping them navigate the complexities of retirement planning in volatile markets. By focusing on preserving wealth, managing risk, and optimizing growth opportunities, we provide tailored strategies that aim to protect your retirement income, even in uncertain times.

The Importance of Long-Term Perspective

Market volatility is inevitable, but it doesn’t have to derail your retirement plans. One of the most important things you can do is maintain a long-term perspective. The stock market has historically recovered from downturns and rewarded patient investors. For example, despite the dramatic declines seen during the 2008 financial crisis, the market went on to deliver strong returns over the following decade.

In retirement, it’s not about avoiding risk altogether but managing it wisely. By creating a well-balanced portfolio that includes a mix of assets and maintaining a long-term perspective, you can better withstand periods of market turbulence.

How CKS Summit Group Can Help

At CKS Summit Group, we’re experienced in providing tailored financial strategies for high-net-worth individuals nearing retirement. Our team understands the unique challenges that come with market volatility and is dedicated to helping you preserve your wealth and achieve your financial goals. Here’s how we can assist you:

- Retirement Income Planning: We help you create a sustainable income plan for retirement, helping ensure that your assets are effectively positioned to meet your financial needs throughout your golden years.

- Wealth Management: Our personalized financial planning services take into account your specific needs and goals, helping ensure a holistic approach to retirement planning.

- IRA & 401(k) Rollovers: Our advisors guide you through the rollover process, helping ensure that your retirement accounts are optimized for growth and tax efficiency.

- Legacy Planning: We assist you in developing strategies to protect and transfer your wealth to future generations, helping ensure your legacy is preserved according to your wishes.

- Asset Protection: We implement strategies designed to help safeguard your assets against potential risks, providing you with peace of mind.

- Tax-Efficient Strategies: Our team works with you to identify tax-saving opportunities, helping to enhance your overall financial strategy while minimizing your tax burden.

With years of experience in wealth management, our advisors are committed to acting in your best interest, providing the knowledge you need to make informed decisions during uncertain times.

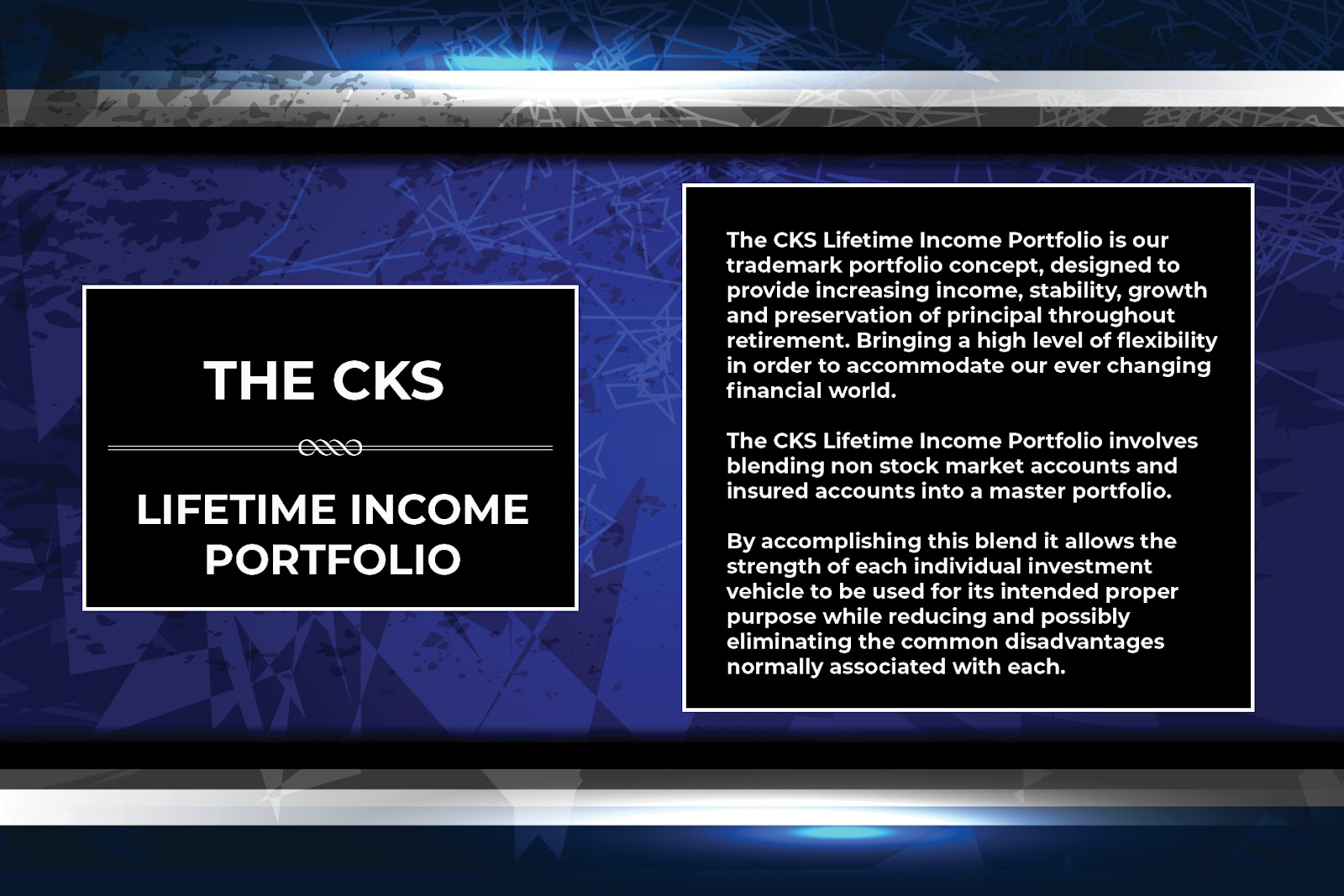

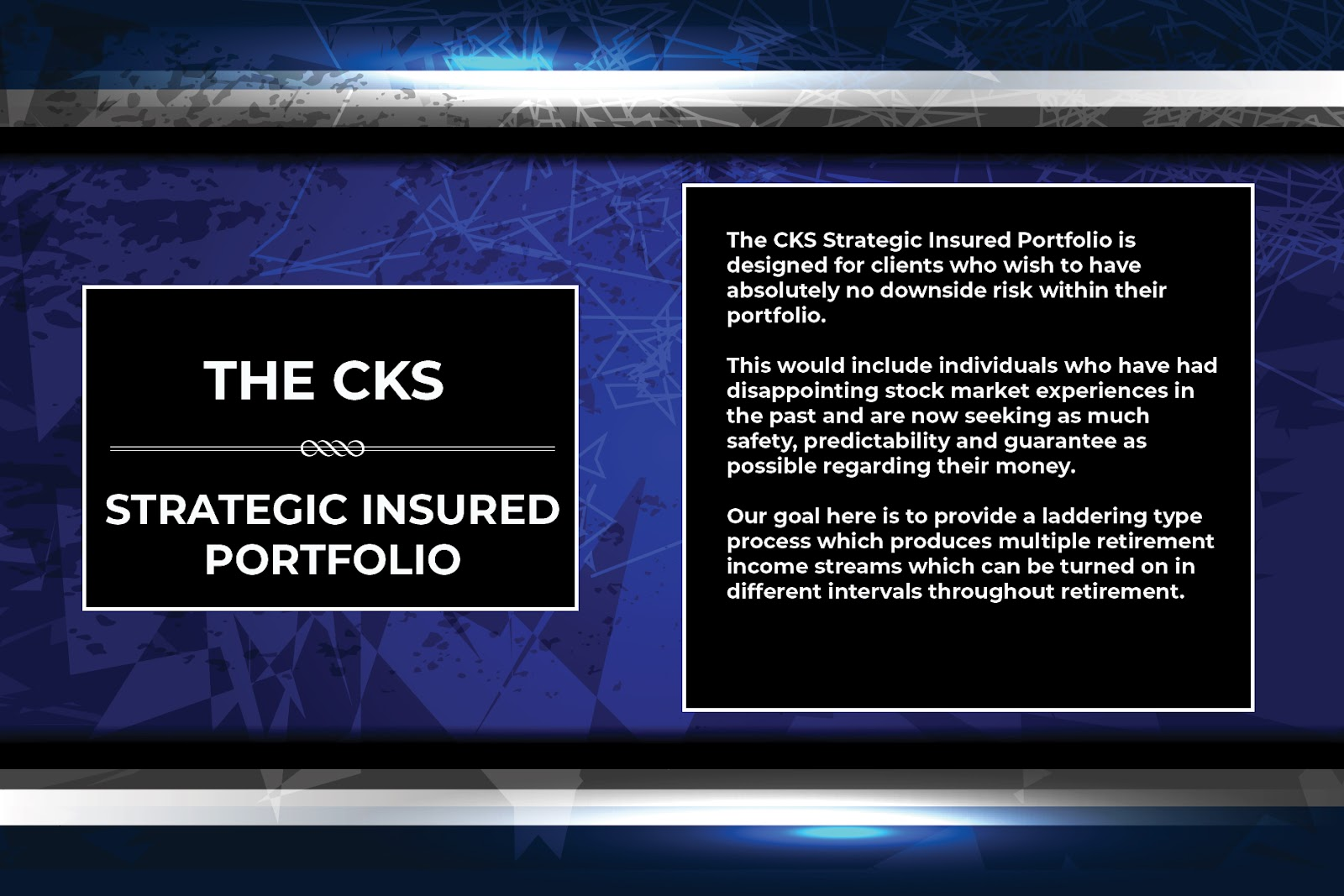

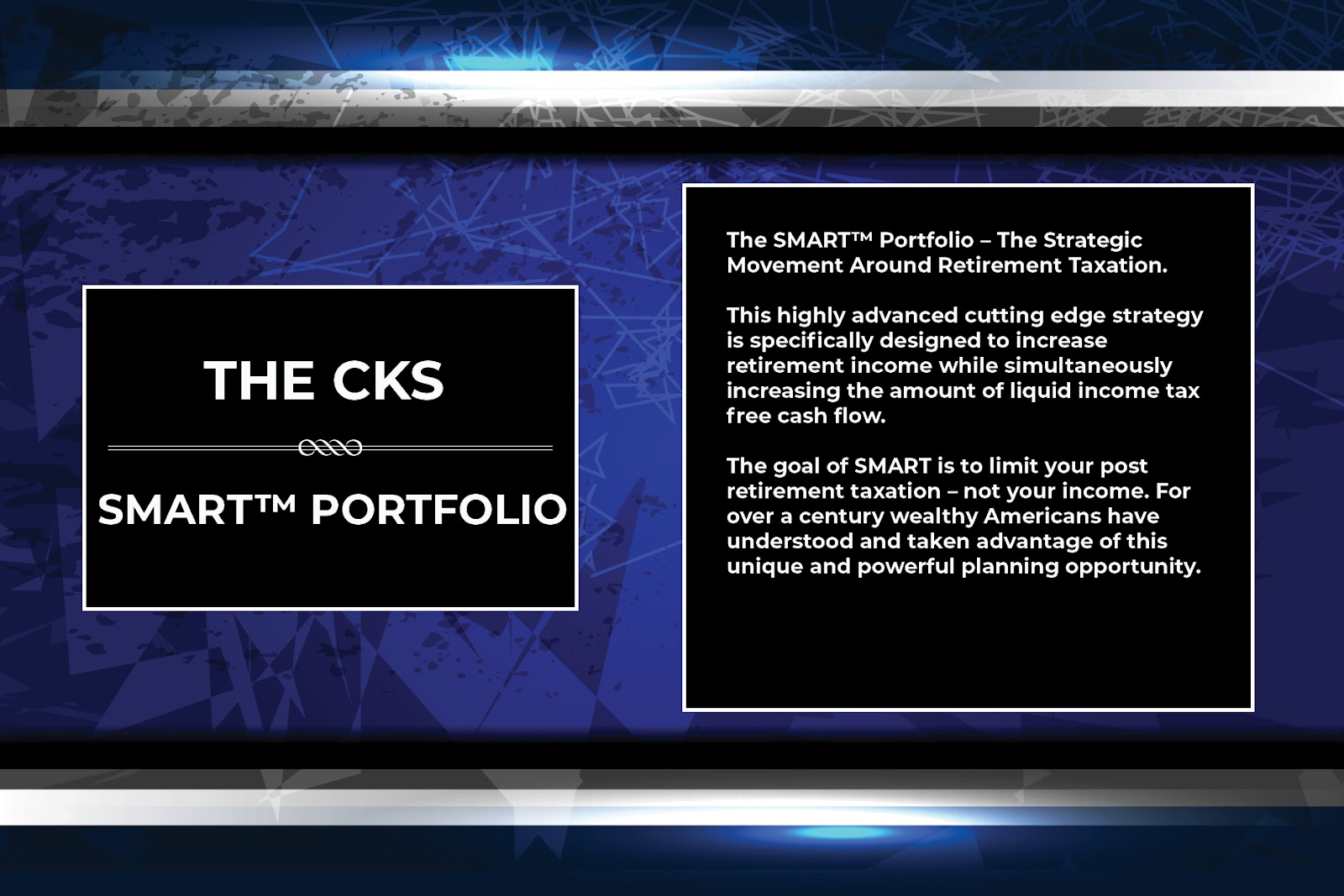

Our Portfolio Options

Final Thoughts

Market volatility can be a cause for concern for those approaching or in retirement, but it doesn’t have to spell disaster for your retirement savings. Diversifying your portfolio, reassessing your risk tolerance, adopting strategies like the bucket method, and working with a trusted financial advisor can help you mitigate the impact of market swings and preserve your wealth for the future.

At CKS Summit Group, we understand the unique challenges that market volatility poses to high-net-worth individuals nearing retirement. Our team is dedicated to helping you develop a retirement plan that focuses on minimizing risk, maximizing income, and helping ensure that you can enjoy your golden years with confidence.

To learn more about how CKS Summit Group can help you protect your retirement savings in today’s volatile market, visit us at summitgp.com.

Retirement Planning FAQs

1. How much should I save for retirement?

The general rule of thumb is to aim for saving at least 15% of your income annually, but this can vary based on your desired retirement lifestyle, age, and current savings. Many financial advisors suggest having 10 to 12 times your final salary saved by retirement.

2. What are the best retirement accounts to use?

Common options include 401(k) plans, traditional IRAs, and Roth IRAs. Each has its own tax advantages, contribution limits, and withdrawal rules. The best choice depends on your income level, tax situation, and retirement goals.

3. How can I estimate my retirement expenses?

To estimate retirement expenses, consider your current living expenses and adjust for any changes you anticipate, such as healthcare costs, travel, or housing. A common method is to plan for about 70-80% of your pre-retirement income annually.

4. When should I start taking Social Security benefits?

The best time to start taking Social Security depends on your financial situation and health. You can begin as early as age 62, but waiting until your full retirement age (or later) can increase your monthly benefits. It’s important to evaluate how this decision fits into your overall retirement plan.